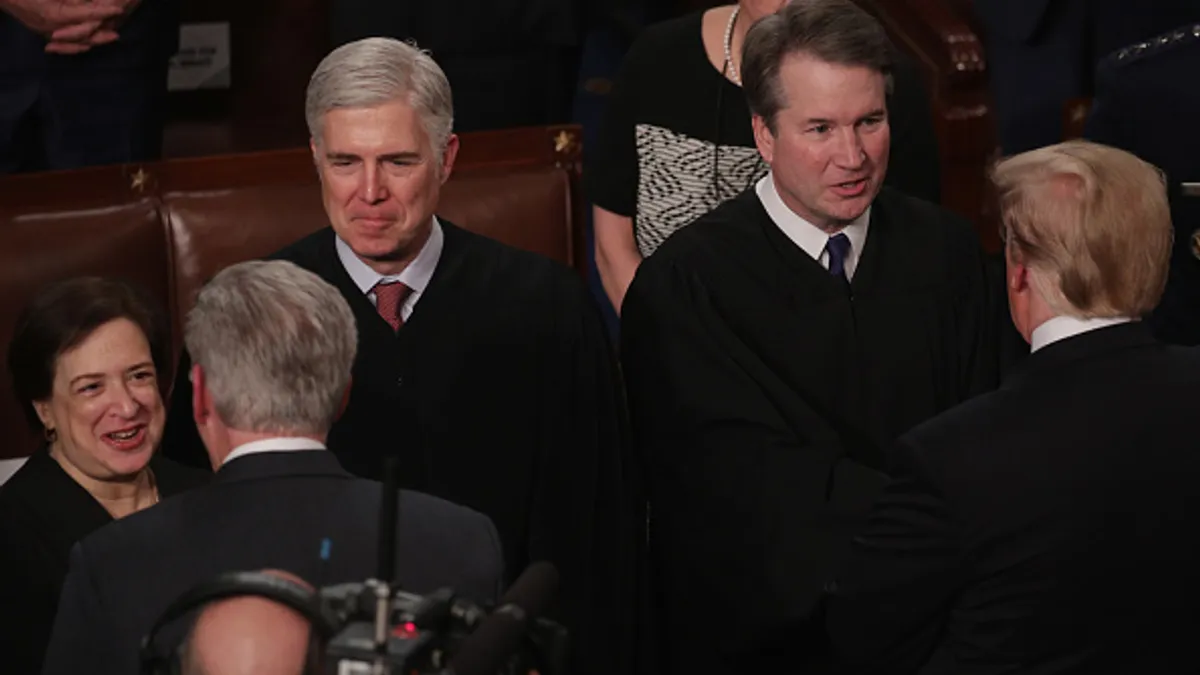

The Supreme Court on Thursday upheld, by a 7-2 vote, the Consumer Financial Protection Bureau’s funding structure — in effect, ending an argument that threatened to dismantle the agency.

At issue was the process wherein the CFPB receives its appropriations through the Federal Reserve, not Congress. A pair of trade groups, the Community Financial Services Association of America and the Consumer Service Alliance of Texas, sued the CFPB in 2018 to void the agency’s rules that bar payday lenders from automatically drawing payments from borrowers’ bank accounts.

The 5th Circuit Court of Appeals in 2022 dismissed many of the trade groups’ points but agreed that the CFPB’s funding apparatus violates the U.S. Constitution’s separation-of-powers principles. The 2nd U.S. Circuit Court of Appeals, by contrast, found the CFPB’s funding structure constitutional, in a March 2023 ruling, setting up the Supreme Court showdown.

“The Bureau’s funding does not violate the Appropriations Clause,” Justice Clarence Thomas wrote for the majority Thursday.

That a Republican justice wrote the opinion defending the CFPB is significant, too. The Supreme Court has heard arguments regarding the bureau before. In 2020, the court ruled 5-4 — along party lines — that the president could fire the CFPB director “at will,” not just for cause.

Democrats typically have argued the agency’s distance from Congress helps keep its focus on consumers. Republicans, meanwhile, often brand the bureau as a maverick agency that meddles with the free market.

“Despite the setback from today’s ruling, Republicans will continue the fight to rein in the rogue CFPB,” Rep. Patrick McHenry, R-NC, said in a statement Thursday.

McHenry, the House Financial Services Committee chair, urged support for a legislative fix to the funding structure — a bill that’s meant to “fix the mistakes of Dodd-Frank, which set the dangerous precedent of tapping the central bank to fund partisan political objectives.”

Sen. Elizabeth Warren, D-MA, lauded the decision Thursday, saying the CFPB is “here to stay.”

“This isn’t the last attack on the CFPB we’ll see from Wall Street, the banks and their Republican allies,” said Warren, the bureau’s architect. “When an agency is this effective at sticking up for working families against industry’s consumer abuses, it’s an obvious target for multimillion-dollar lobbying campaigns. The CFPB will keep on doing its work to slash junk fees, fight giant banks when they cheat people, and level the playing field for everyone in this country.”

The Supreme Court may have showed its hand in October, when it heard oral arguments in the case. Several justices — Republicans among them — spoke skeptically toward the payday lending groups’ assertions.

“Congress has not determined the amount that this agency should be spending,” Noel Francisco, the former solicitor general who served as the groups’ lawyer, told the Supreme Court last fall. “Instead it has delegated to the director the authority to pick his own appropriation subject only to an upper limit that’s so high, it’s rarely meaningful.”

“I think we’re all struggling to figure out, then, what’s the standard that you would use,” Justice Amy Coney Barrett, a Trump appointee, asked Francisco. “How do you decide how much is too much or how specific is specific enough?”

The CFPB’s funding structure, Francisco argued, allows the CFPB to dip into a “perpetual” stream of funding.

Justice Brett Kavanaugh, another Trump appointee, dismissed that notion.

“Congress could change it tomorrow, and there’s nothing perpetual or permanent about this,” he said.

Barrett and Kavanaugh voted with the majority Thursday, along with Thomas, Chief Justice John Roberts and the court’s three Democrats: Sonia Sotomayor, Elena Kagan and Ketanji Brown Jackson. Justices Samuel Alito and Neil Gorsuch dissented.

“There is apparently nothing wrong with a law that empowers the Executive to draw as much money as it wants from any identified source for any permissible purpose until the end of time,” Alito wrote in his dissenting opinion. “The CFPB enjoys a degree of financial autonomy that a Stuart king would envy.”

Thursday’s decision also likely means forward motion on CFPB objectives that have been in somewhat of a holding pattern — specifically, a small-business data collection rule that a district court judge put on hold last fall pending the outcome at the Supreme Court.

But the CFPB likely also will gain confidence that its more recent proposals — on open banking and overdraft fees — could see less fervent pushback.

Still, at least one trade group, the Consumer Bankers Association, noted Thursday’s ruling “should not be considered a popular endorsement of the CFPB’s recent and seemingly political rulemakings, many of which have skipped important legal requirements and have raised concerns under the Administrative Procedure Act.”

“Any agency, even if its funding is constitutional, is unfortunately capable of engaging in rushed and ill-conceived rulemakings, as the CFPB has recently,” the CBA said, adding, though, that it is “heartened that this important legal question has been resolved.”